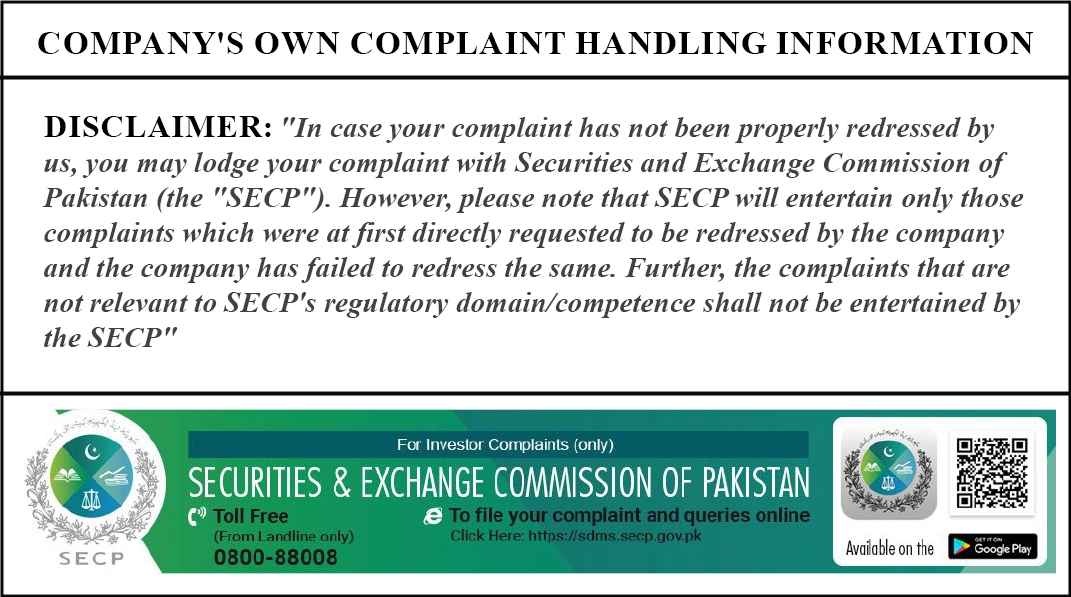

Lucky Islamic Punjab Pension Fund

- All employees who joined service on or after January 8, 2024 will fall under the new Pension System introduced by the Punjab Government.

- The investment management has been entrusted to registered Pension Fund Management Companies (with Securities & Exchange Commission of Pakistan), including Lucky Investments Limited.

- Fund will be governed under Voluntary Pension System Rules, 2005, Non-Banking Finance Companies Regulations & Notify Entity Regulations, 2008 and Punjab Defined Contributory Pension Scheme Rules, 2025 including all other applicable laws.

- Each employee has the right to choose the Pension/Asset Management Company of their preference and investment mode (Conventional or Shariah complaint) through the portal: https://pension.punjab.gov.pk/ after completing the profile. (Note: Lucky Investments Limited offers only Shariah complaint options)

- Employee needs to complete his/her profile on https://pension.punjab.gov.pk/ portal, upon verification, information will be passed on to Pension/Asset Fund Management Company for account opening.

Govt. of Punjab had amended the Punjab Civil Servants Act, 1974 (VIII of 1974) (through Punjab Civil Servants Ordinance, 2023

(1 of 2024) and introduced Punjab Defined Contributory Pension Scheme Rules, 2025 and the Pension structure has been changed for all new Punjab Govt. employees after the notification.

Life Takaful Cover:

The pension account holders will receive built-in Group Life Takaful benefit of PKR 1,000,000 on Death/Permanent Disability before attaining Retirement Age. In Case of Accidental Death before attaining Retirement Age Group Takaful benefit will be of PKR 2,000,000. Provided further that the Group Life Takaful benefit limit specified above shall be subject to annual indexation up to 10% for all employees, both those previously insured and those joining within the year and rounded up to the nearest PKR 1,000.

Note: It is clarified that no financial, administrative, or legal obligations will fall on the Pension Fund Manager (PFM) or the Pension Fund regarding the Takaful benefit until the Finance Department, in coordination with the Punjab Pension Fund and MUFAP, finalizes the Takaful arrangement and it becomes fully operational.

Contribution rate:

The Government of Punjab and the employees will each contribute to the pension fund according to the prescribed contribution rates. The employee’s share, calculated on their pensionable pay (current basic salary), will be deducted at source and remitted to the selected Pension/Asset Fund Management Company.

| Monthly Contribution rate (% of pensionable pay) | |

|---|---|

| Employer's Contribution | 12% |

| Employee's Contribution | 10% |

| Overall Contribution | 22% |

Asset Allocation:

For the first three years from the date an employee’s pension account is opened (irrespective of the employee’s age), 100% of contributions will be allocated to Money Market Sub -Funds only. Upon completion of three years, employees may opt for a customized asset allocation, subject to the following limits:

| Age of Employee | Aggregate exposure limit | |||

|---|---|---|---|---|

| Equity Index Sub-Fund | Equity Active Sub-Fund | Combined Exposure to Equity | Debt / Money Market Sub-Fund | |

| For 3 Years from date of pension account opening | 0% | 0% | 0% | 100% (Money Market Sub-Fund Only) |

| Up to 30 Years | Max 50% | Max 25% | Max 50% | Min 50% |

| Up to 40 Years | Max 40% | Max 20% | Max 40% | Min 60% |

| Up to 50 Years | Max 30% | Max 15% | Max 30% | Min 70% |

| Up to 60 Years | Max 20% | Max 10% | Max 20% | Min 80% |

Maximum aggregate Exposure Limit:

In case, an employee does not specify their preferred allocation policy, the age-based default asset allocation will be applied automatically after the initial three-year period (regardless of the employee’s age).

| Age of Employee | Aggregate exposure limit | |||

|---|---|---|---|---|

| Equity Index (High Risk) | Equity Active (High Risk) | Debt (Medium Risk) | Money Market (Low Risk) | |

| For 3 Years from date of pension account opening | 0% | 0% | 0% | 100% |

| Up to 30 Years | 30% | 10% | 30% | 30% |

| Up to 40 Years | 20% | 10% | 30% | 40% |

| Up to 50 Years | 15% | 5% | 20% | 60% |

| Up to 60 Years | 10% | 0% | 10% | 80% |

Retirement Age:

Retirement age of an Employee shall be such date as given below:

- The date after the participant/employee completes twenty years of service qualifying for pension or other retirement benefits, if the competent authority, in the public interest, direct; or

- in the absence of direction given under clause (i) on the completion of the sixtieth year of his age.

- or any date as specified under Punjab Civil Servant Act 1974.

Transfer to another Fund/Pension Fund Manager:

Participants shall be entitled to transfer his pension account in accordance with the terms of the Offering Document the whole of their Individual Pension Account with the Lucky Islamic Punjab Pension Fund to a pension fund managed by another pension fund manager with whom the Employer has made similar arrangements.

Withdrawal Conditions:

- Participants cannot withdraw any amount from their pension account before reaching the designated retirement age.

- If a participant leaves service before attaining retirement age may, by notifying in writing to the Punjab Pension Fund, choose to discontinue participation under the Punjab Defined Contribution Pension Scheme Rules, 2025. In such a case, the participant may either transfer their pension account balance to another employer’s pension fund or withdraw the accumulated balance, subject to the VPS Rules, 2005 and all other applicable laws.

Options available to participants upon retirement:

- Participant may withdraw up to 25% of the balance from their Individual Pension Account; and

- To use remaining balance to purchase an annuity from a Takaful Company or Pension Fund Manager, of the participant’s choice.

- Participants may enter an Income Payment Plan (IPP) with the Pension Fund Manager, allowing monthly withdrawals from the remaining balance for:

- A minimum tenure of 20 years, or

- Until the participant’s death, whichever is earlier.

Withholding tax will be deducted on any early withdrawals made before the eligible retirement age of 25 years from the date of joining such scheme or before the age of 60, whichever is earlier, in accordance with the Income Tax Ordinance, 2001.

Disclaimer – Tax Credit u/s 63 of Income Tax Ordinance, 2001 on sources of income from “salary” and “business income” on investment up to 20% of taxable income can be availed on contributions made in any tax year. Currently there is no Capital Gains tax on units of pension fund and WHT on dividends, also there is no requirement for distribution dividends from Pension sub-funds. Income from Annuity & Income Payment Plans is subject to income tax as per Income Tax Ordinance, 2001.